What Will Inflation Do to Bitcoin?

What Will Inflation Do to Bitcoin?

A little inflation goes a long ways

Last week Fed chair Jerome Powell gave his annual state of the economy speech. He promised more money-printing, suggesting the Fed will remain the government’s piggy bank for awhile yet.

This raises concerns about inflation in future, so this week’s question is how much inflation does it take to make Bitcoin go up a bunch.

The answer: a little goes a long ways.

How does inflation affect Bitcoin?

The simplest model relating how many dollars exist and how much stuff costs is the Quantity Theory, which says that every price in the economy tends to move with the number of dollars in existence. So if the Fed doubles today’s money supply, then every price tends to double. A $3 Happy Meal goes to $6, a $200,000 house goes to $400,000, and today’s $50,000 Bitcoin goes to $100,000.

Of course, this is a massive oversimplification for many reasons, from “inflation illusion” to Cantillon Effects. So a more interesting approach is to look from the perspective of the investors themselves -- the people who are actually placing buy or sell orders.

Here, there’s a very interesting feature to inflation hedges, which is that they over-react massively. If, indeed, Bitcoin is replacing gold as the go-to inflation hedge, then recent history says a little inflation may make Bitcoin go up a ridiculous amount.

How ridiculous? Let’s look at America’s last two major economic crises: the 1970’s inflation, and the 2008 financial crisis.

1970’s Inflation

In the 1970’s, Richard Nixon took the dollar off gold, causing rampant inflation. That inflation was initially, like today, blamed on idiosyncratic or temporary factors, including the worldwide population boom that would make us run out of stuff and fall off the planet. By the way, that foolishness should give us pause that the Fed will, once again, fail to recognize real inflation when it comes.

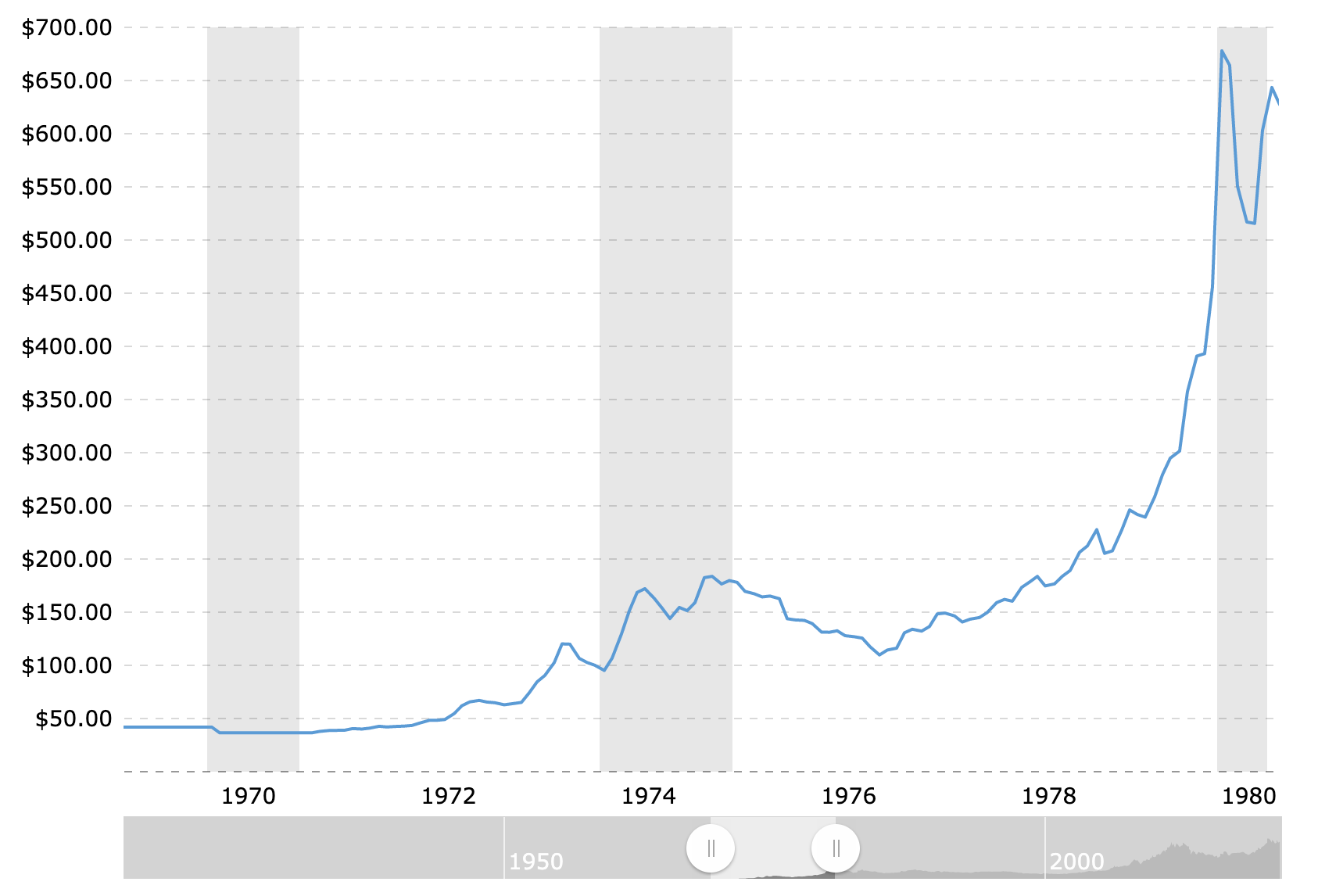

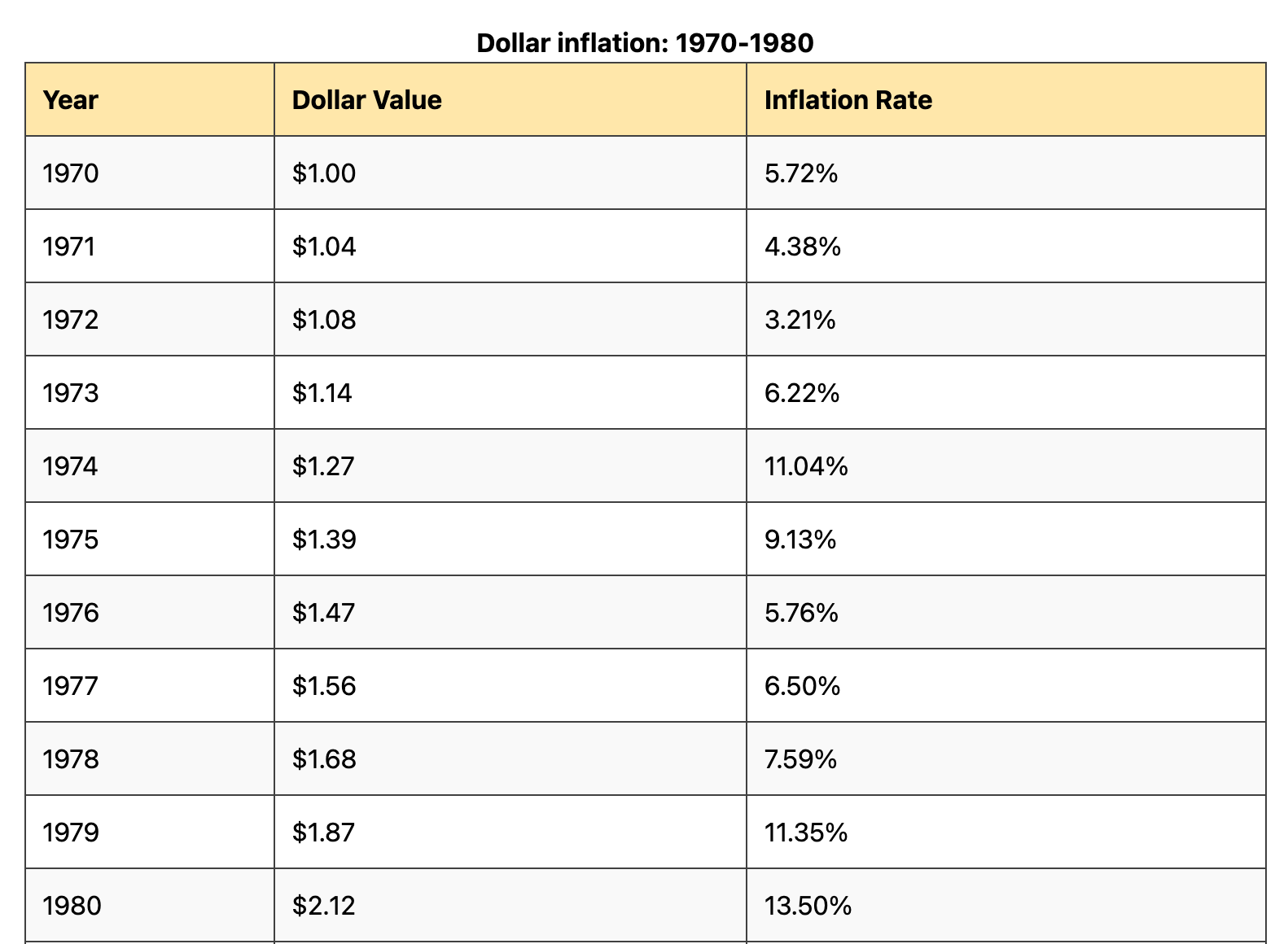

At any rate, over the 1970’s, price inflation averaged 7.8% per year, for a cumulative rise in consumer prices of 112%. This meant something that cost $1 in 1970 would cost $2.12 in 1980. So your dollar in 1970 only bought 47 cents worth of stuff by 1980. And yet gold didn’t just double, it went to the moon: from $37 in January of 1970 to $678 in January of 1980 – a nearly 20-fold gain.

Why did gold rise so much? Because gold was the backup plan – the “insurance policy” for individuals. After all, simply adjusting by price inflation would have taken gold up 112% from $37 to $78 – a $41 gain. The other $600 was extra. It was coming from inflation, to be sure, but in the form of personal insurance against a crash.

So, using the 1970’s as a natural experiment, that personal insurance accounted for, in dollar terms, a 15 times greater jump than the inflation itself.

Interestingly, this bet wasn’t on governments going back to gold. Why do we know this? Because the peak price of gold before the Nixon Shock had been $42. Not $678. If, in fact, the market was simply betting on Nixon going back to gold, it should’ve returned to $42, not soared nearly 20-fold.

So why did it overshoot so hard? Because there are a lot more individuals than there are central banks.

Essentially, from investors’ perspective, Nixon had taken us from a world where the central bank sort of protects your money to a world where it’s every man for himself. Metaphorically, Nixon took us from a town with one, big lock on the city gate to a town with 100,000 individual locks on every single door and window.

Even if that big lock hadn’t been doing a super job, ask what would happen to the price of locks if everybody suddenly needs one. Especially if gold, metaphorically, was the lock. Incidentally, Nic Carter recently wrote about this phenomenon in Bitcoin magazine, in the context of gold’s relentlessly rising energy use.

So, taking the 1970’s as a natural experiment, a small change in inflation can lead to a much larger change in the price of the inflation hedge.

2008 Financial Crisis

The next big crisis was in 2008. Inflation wasn’t the driver here, rather it was fear about a repeat of the Great Depression. After all, the 1930’s Depression also started with Wall Street imploding.

In 2008 gold was again the hedge of choice, since Bitcoin didn’t exist yet. In fact, Satoshi’s white paper didn’t come out until October of that year, 2 months after Lehman Brothers imploded. In fact, the very first Bitcoin block references the bailouts themselves.

Meanwhile, the first recorded Bitcoin transaction wouldn’t even come until 2010, when a hungry bitcoiner bought some pizza.

So 2008 was still all about gold.

And what did gold do when people feared Depression? Same picture: gold went from $1,100 in August, 2008 to nearly $2,200 just 3 years later. Meanwhile, cumulative inflation in the those 3 years had been under 5%. So, again, the jump in gold outperformed the move in inflation by roughly 20 times – a 100% gain for a 5% change in inflation.

Interestingly, the main fear in 2008 was economic – GDP growth – not inflation per se. The story went that if Wall Street implodes, America would plunge into chaos, with soup kitchens, rummaging through garbage for dinner, hobos killing each other for thigh meat. I think this was bullshit to scare the public into bailing out Wall Street, but the point stands that people weren’t worried about inflation per se, they were worried about growth and wealth destruction.

So, summarizing, in both the last inflation crisis and the last growth crisis, gold moved an order of magnitude more than it should have from a top-down Quantity Theory count.

Covid-19 Crisis

And that brings us to today’s crisis. The first crisis where Bitcoin, finally, does exist.

Covid-19 should have been the perfect storm for gold, pairing 2008 existential dread with runaway money creation that is, in just 18 months, already giving us the specter of 1970’s inflation. It should have been gold’s moment to really shine.

Was it?

Going to the tape, early in the crisis everything plunged, including gold and Bitcoin. This is normal in a crisis – people panic and want to hold lots of cash in case they need it for toilet paper or to flee to Montana.

So we can start the clock from June, 2020, about 4 months in, as that moment when consumer prices leveled off then started rising. At that point, gold was going for just under $1,800 per ounce, while Bitcoin was worth $9,889.

Now, 15 months later, where do our hedges stand? Bitcoin, clearly, picked up crisis-level demand, jumping 5x to now bumping around $50,000.

And where is gold? Why, it’s still at $1,800 per ounce. Well, $1,817.92 as of this moment. So 1% -- a loss in inflation-adjusted terms.

So far, then, Bitcoin has done what a hedge should do in a crisis. While gold has done… nothing.

Now, the big question from here is whether we’re seeing the early stages of a rotation, where Bitcoin replaces gold as crisis hedge. Or if, instead, Bitcoin’s rising for its own idiosyncratic reasons while gold’s still asleep because this isn’t a real crisis and gold’s bored.

The bored gold narrative strikes me as very unlikely given the terrible GDP numbers, terrible inflation numbers, and the fact the public has been demonstrably less chill than in previous crises — just ask the toilet paper. So, no, gold should be rising, and the fact it isn’t means something changed in investor demand.

So my guess is that, indeed, Bitcoin is picking up the personal insurance demand that used to flow into gold. Like a tsunami up a canyon, that insurance used to make gold go to the moon, and now it’s doing it to Bitcoin.

Still, I think it’ll take time — paraphrasing Max Planck, Bitcoin understanding proceeds one funeral at a time, as the elderly go to investor heaven and are replaced by Bitcoin-savvy whippersnappers. Still, I’m surprised how dramatic the divergence has been this early.

What’s Next for Bitcoin?

So what comes next? Economically, the big questions are whether growth recovers, and whether inflation runs away. I’ll go through those 4 scenarios in depth in another article (subscribe free here) but, in short, if the administration or the Fed screws up, Bitcoin probably goes up a lot.

Both this administration and this Fed strike me as particularly incompetent, so I think those pro-Bitcoin scenarios are pretty likely.

Finally, throughout all this, keep in mind that crisis demand is just one piece of Bitcoin’s demand. Compared to gold, Bitcoin’s big-picture is probably far more dominated by onboarding of millions of new users, by supply dynamics like stock-to-flow ratio, or by myriad regulators all over the world either giving up on regulating Bitcoin or even switching sides and promoting Bitcoin.

So, panic-demand or not, Bitcoin will likely continue to march up. Whether in sunshine or in rain.

Thanks for reading, and subscribe for weekly updates. See you next time!

Now - in Poland we have high inflation.. Maybe invest crypto for safe? :P Check our blog! https://chairpc.pl